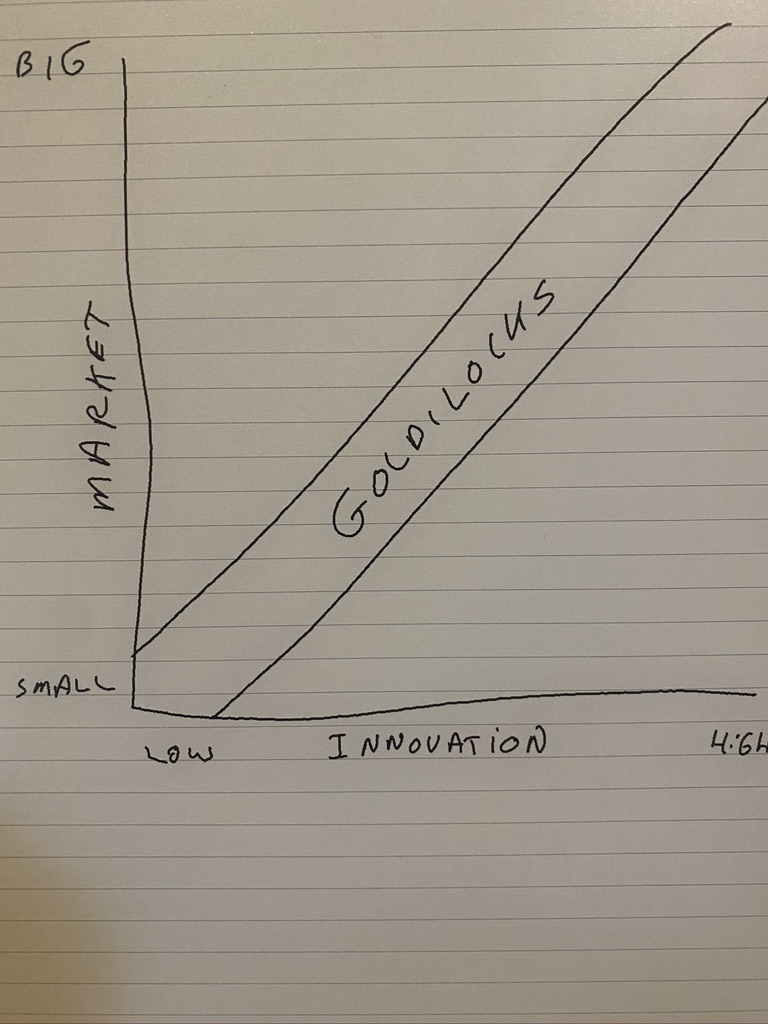

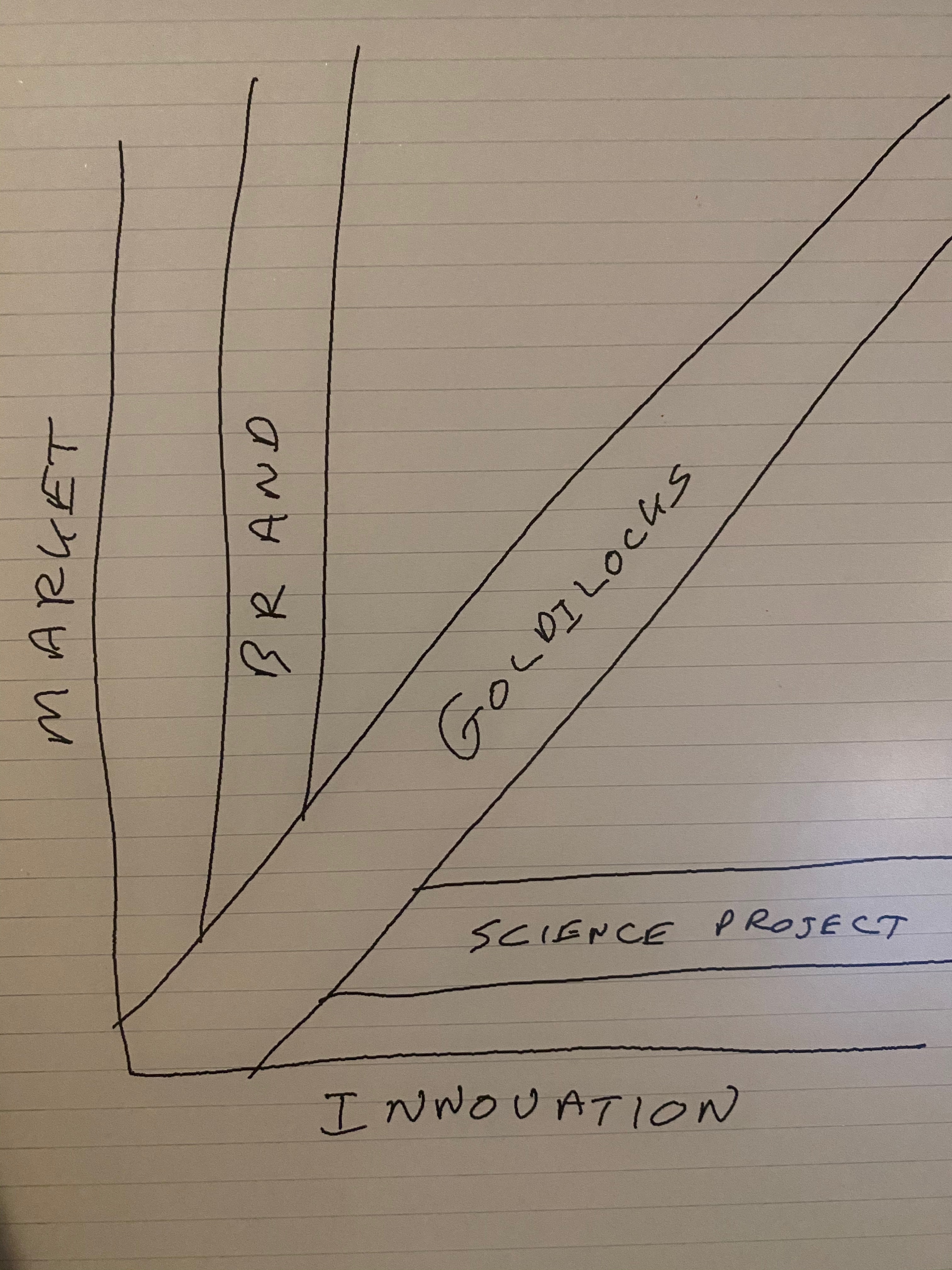

Goldilocks: Adjective: “having or producing an optimal balance usually between two extremes.”

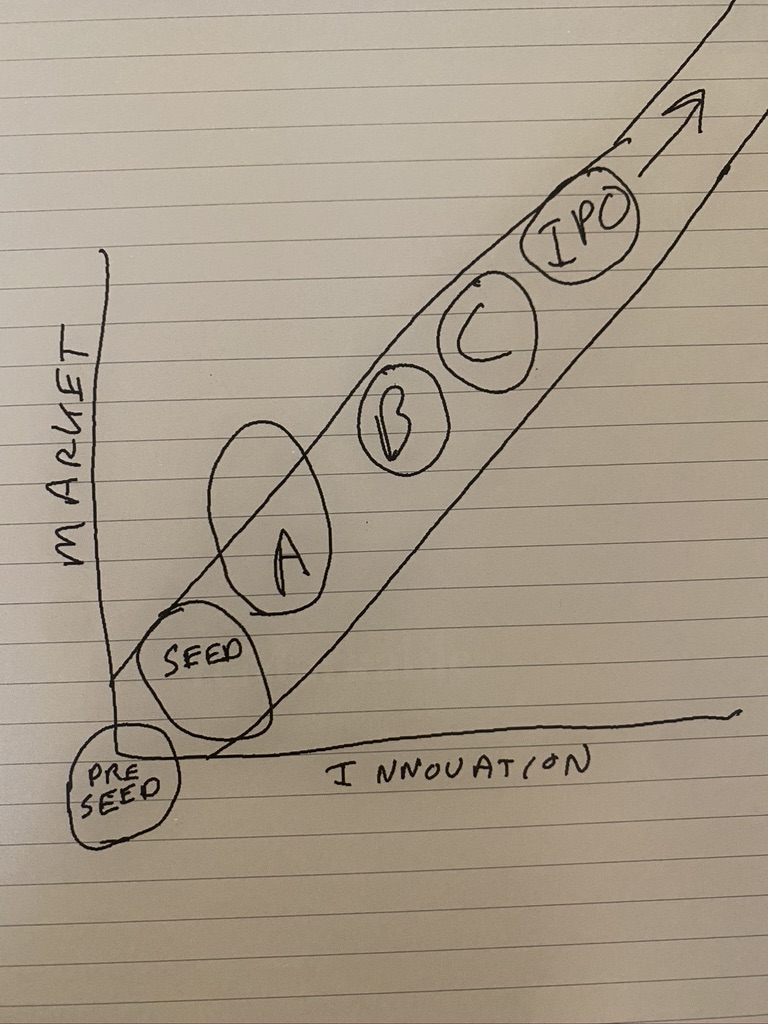

I am often asked “What stage do you invest?” While most people expect to hear “Pre-Seed”, “Seed” or “Series A, B, C, etc”, I answer “The Goldilocks Stage”. Traditional Venture stages have become a function of fund size and seem to be increasingly disconnected from any thesis around long term value creation. When you start to look for the Goldilocks Stage, you will find it everywhere; Early-stage venture, mid-stage, Growth stage, IPO, and the public markets.

Every investment I have ever made with a 10x or more return was in the Goldilocks Stage. Here is how I define it:

- Goldilocks Stage: “The “just right” mix of value-creating innovation balanced with a clear path to profitably fulfilling a fast-growing customer need.”

When you invest in the Goldilocks Stage you fund a clear set of milestones intended to move the company up the path of product innovation and customer adoption to the next logical inflection point. In the Goldilocks Stage Innovation = Customers. The ultimate goal of every company which hopes to continue to grow should be a self funding loop of Innovation = Customers = Innovation = Customers…. ad infinitum. For a master class on this see: Amazon, Apple, Google, Tesla, etc. Companies stall when they either stop innovating or fail to find new customers. For a master class on this see: General Motors, General Electric, most Oil majors, etc.

Less than 5% of the deals we see at Incisive Ventures are raising funding in the Goldilocks Stage targeted at BOTH customer and innovation growth. Many VCs are mainly funding ONE side of the equation which, while it may lead to up rounds, rarely leads to long-term sustainable growth and the virtuous self-funding cycle. Make these one-sided investments at your peril.

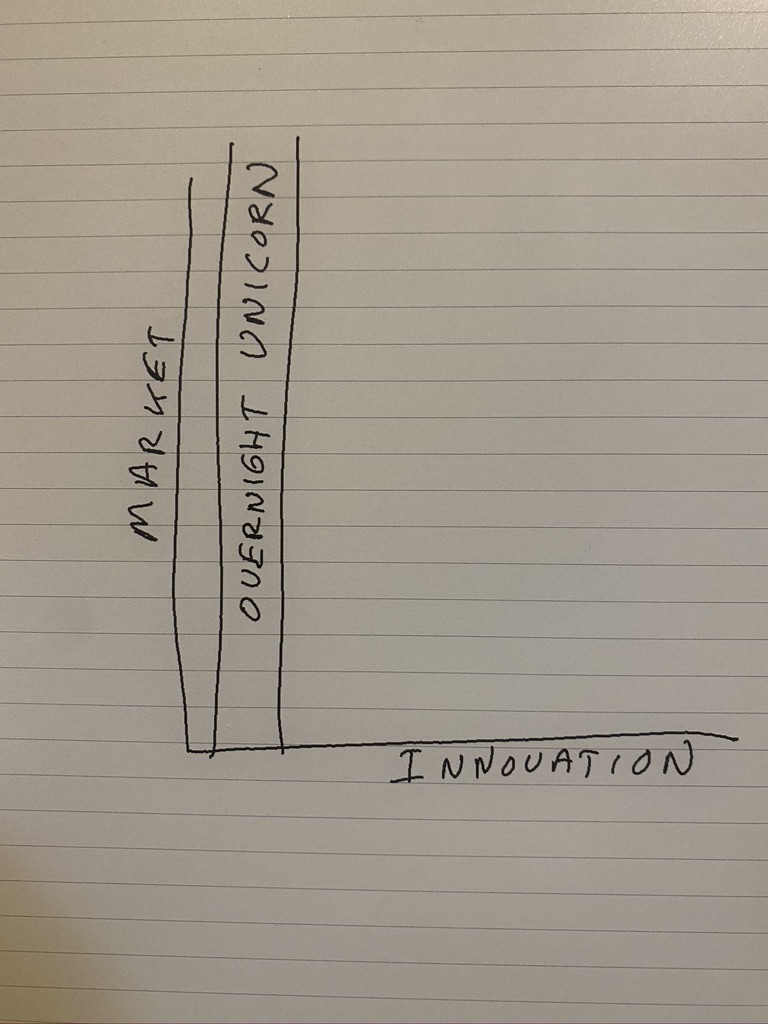

Two scenarios we commonly see (and DO NOT INVEST IN) include:

The Overnight Unicorn or Brand Project.

In this scenario, minor innovation gains wild adoption quickly. With massive adoption numbers, investors pour funds into customer acquisition and expansion, oftentimes before the business model has been fully flushed out. While there have been many examples of investors making money in these deals, most have flamed out when customer growth stalled and there was no new innovation to reach new customers.

Examples include:

- Bird. One of the fastest companies to >$1B valuation in the history of venture. Investors funded an aggressive expansion based on initial traction. The innovation was very thin: Off the shelf scooters with a booking/billing app and some access control hardware. Investors funded brand building and building the network over innovation.

- Honey. Making a browser plugin that automatically tried coupons was a very thin innovation, but it got massive customer adoption because it removed all the searching, copy and pasting of coupons (the friction). Investors piled in behind huge adoption numbers.

- WeWork. Co-working was around long before WeWork. There was little technology innovation and heavy investment in brand and fund negative returns to gain customer share, hoping to make it up in the end.

The primary risks in Overnight Unicorns include:

- Lots of competitors. Since there is little innovation, these concepts can be copied easily and must rely on brand and customer loyalty for profits. With lots of competitors, margins get squeezed and many times no-one in the category is making profits.

- Stalled customer acquisition. Either because the market gets saturated, or because competitors come in and compete for customers. When the valuation is based on rapid customer growth, and that stalls, even reverts, bad things happen.

The right kind of Overnight Unicorns:

- The power law in venture investing gains much of its power from the fact that companies creating new categories, tend to get an outsized percentage of the market and valuation multiple. If a company is truly creating a novel category, sometimes focusing on customer/market share is the right initial strategy when balanced with delivering innovation over time which delivers increasing value to the market.

- A classic example of this is Facebook. They focused on fairly simple community technology at first and drove massive audience growth. When they went public they had barely turned on advertising. They kept up the innovation internal and through M&A (WhatsApp, Instagram, etc.) as the audience also grew. This pushed the company back into the Goldilocks stage.

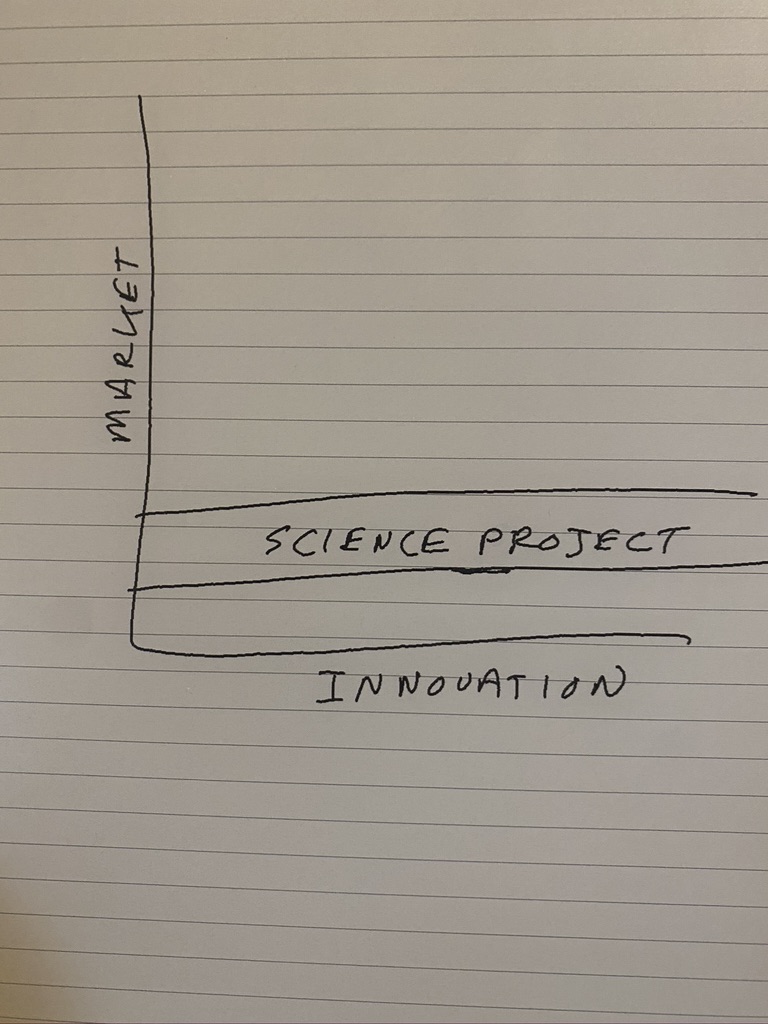

The Science Project.

In this scenario, the company falls down a feature rathole or bites off a problem too expensive to solve within their funding window versus the value delivered. Valuation is driven by product progress, patents, hiring smart people, etc. rather than customer traction. One can also find cases where investors made returns with science projects, it is typically through acquisition by a company with access to customers rather than as a stand-alone entity. There have also been spectacular flameouts when the end product could not profitably find a large enough market. Product development always costs more and takes longer than the budget, these deals can easily outrun their funding runway.

Examples include:

- Virgin Galactic. The story has romantic appeal, the founder is charismatic, they have been at it for 10 years and don’t have a clear path to success. Even if they can successfully fly, how big is the market for space tourism really?

- Nikola Motors. Another appealing story is “The Tesla of trucks” with a charismatic founder. But building trucks is hard, they can’t decide on the fuel source, outsource most of the production, and there are weird accounting things. Oh and Tesla has its own commercial truck planned and a track record of delivering products (albeit a bit late).

- Theranos. Sometimes when developing a very hard product, the pressure to show progress can be so great that companies actually lie to investors. Investors believed the made up progress and promise of big market. The product never worked. We know the ending.

- Juiceroo. I was never lulled by the idea of a $400 juice box squeezer. Plenty of others were. I love the hardware teardown which exposed how over-engineered the device was. Copious investor dollars spent to do something the human hand could do for free.

The primary risk in Science Projects include:

- Overrunning the funding window. If you can’t ship a product on the capital you have raised, you depend on investors to believe more development will lead to a product in the future. Cost overruns can ruin a funding window.

- Building the wrong product. Without customer feedback, engineers build what they think the market wants, or more typically what they want. There is often a disconnect.

- Not getting final approvals. Many products, even if they work, require regulatory or market approvals to go on sale. Often companies don’t budget for this step correctly. Or the regulators require re-work, more tests, more trials, etc. driving up product development.

- A scientist who can’t sell. Doing science and selling are very different worlds. When a product is finished and the company pivots to selling, many times they put the scientist in front of customers, which only works in certain industries. Managing product development is very different than managing sales. It is hard to be great at both.

- Market changes during development. I was once an investor in a software company building an operating system for a new class of Intel network operating chips. The company had a contract with Intel to install the software on all chips. But Intel ran into manufacturing and scaling problems with the chips and canceled the project. No chip, no software, no possibility to pivot. More frequent is that someone else solves the hard problem in a different way, or before your product is finished and gets to market before you. Then you are not the innovative leader, you are following. Remember the Sony BetaMax which was way better than the VHS recorder? Didn’t matter, the VHS solved recording TV around the same time in a cheaper and more easy to use way. Problem solved, superior engineering be damned.

The right kind of Science Projects:

- Science projects must eventually deliver a product that customers value, are willing to pay for, and that product must reach customers at a level which overcomes the development costs. There are typically two ways to achieve this:

- Sell to a company with market access. This is the primary business model of biotech firms. Do science for years, then sell to big Pharma who has sales reps to reach the market and get regulatory approval. For a long time this was also the model in networking equipment. Make a new box, sell it to Cisco.

- Get customers. The pivot from science project to selling is very hard. Companies that want to create a self-funding innovation machine need to good at both developing and selling products.

- Be wary of companies that say their patents will be valuable and protect them. There are very few examples of patents creating long term value, too many ways to get around them with a different approach.

Is investing in Goldilocks Stage a guarantee?

No. But I have had better returns over time than any other stage. When writing a check into what they think is a Goldilocks stage, an investor must be right about three things:

- Market trend. The size and shape of the market for the product. How it is growing, how to reach the market, etc.

- Product innovation trend. Can the company build the product given the resources in the round you are investing in. What is the next product? Is there a pipeline?

- Management ability. Can management find the right product/market fit within the funding window you are funding? Have they shown a proven ability to pivot and do what it takes to stay in the zone?

How to identify the Goldilocks Stage?

Spend 25 years angel investing, and you probably will be above average at it. It takes alot of investing in the wrong stage and behind the wrong signals to find the ones that correlate to returns over time. So, yea, make alot of mistakes and learn from them. At the highest level, spend your diligence time on the three areas you have to be right about, market, product, and management. And be right about the FUTURE trends in these areas, do not assume prior performance will continue into the future.

What can go wrong with Goldilocks phase?

You could be (and likely are) wrong about one or all three of the above. The product can stall. The market can stall. Management can fail to execute. Those risks are why you have the opportunity, if right, to make an outsized return.

Many companies start out one way then end up another or go in and out of the Goldilocks phase. Whenever a company presses too hard on one side of the equation at the expense of the other, stalls tend to happen. So ensure progress on both market and product growth while management stays focused on execution.

There is a Goldilocks Stage. It is the “just right” mix of customer traction and product innovation, both of which will continue to grow a meaningful amount during the funding window of the round you are funding. Invest in Brand or Science projects with caution and if you do, have a plan with management to move into the Goldilocks Stage. To follow along with deals Incisive Ventures believes are in the Goldilocks Stage, join us.